Corporate Transparency Act: What You Need To Know To Comply

On January 1, 2024, the federal Corporate Transparency Act (CTA) took effect. This is a new law intended to combat the use of shell companies for laundering money, financing terrorism, and other bad acts by requiring that certain businesses file specific reports with the Treasury Department identifying the businesses owners and management with particularity.

Below is an overview of the requirements to comply with the CTA, including which businesses are affected and what, when, and—importantly—why to file.

Filing Requirements

All businesses that do not qualify for one of the exemptions listed below are required to file a “Beneficial Ownership Information (BOI) Report” with the U.S. Department of Treasury’s Financial Crimes Enforcement Network (FinCEN) via their Beneficial Ownership Secure System (BOSS). BOI Reports are filed electronically at FinCEN’s website: https://www.fincen.gov/boi.

→ FinCEN’s Small Entity Compliance Guide outlines CTA compliance requirements in greater detail: https://www.fincen.gov/boi/small-entity-compliance-guide.

WHO: Businesses Required to File

All corporations, LLCs, and any other business entity formed by filing a document with a secretary of state or similar office (except exempt businesses) and all other business entities formed under a law of a foreign country and registered to do business in any US state (each, a “Reporting Company”), must file a BOI Report, unless they are expressly exempt from the requirement.

The following are the 23 exempt business types:

• Securities reporting issuer

• Governmental authority

• Bank

• Credit union

• Depository institution holding company

• Money services business

• Broker or dealer in securities

• Securities exchange or clearing agency

• Other Exchange Act registered entity

• Investment company or investment adviser

• Venture capital fund adviser

• Insurance company

• State-licensed insurance producer

• Commodity Exchange Act registered entity

• Accounting firm

• Public utility

• Financial market utility

• Pooled investment vehicle

• Tax-exempt entity

• Entity assisting a tax-exempt entity

• Large operating company

• Subsidiary of certain exempt entities

• Inactive entity

Each of the foregoing categories is described in more detail in the CTA: https://www.fincen.gov/boi-faqs#C_2.

Two exemptions warrant further discussion:

→ A “Large Operating Company” is an entity that employs more than twenty (20) full-time employees in the U.S. Business owners are prohibited from consolidating their employee count across multiple entities for purposes of qualifying as a Large Operating Company under the CTA. Each business entity must be evaluated separately.

→ An “Inactive Entity” is one that:

- Was in existence on or before January 1, 2020;

- Is not engaged in active business;

- Is not owned by a foreign person, whether directly or indirectly, wholly or partially;

- “Foreign person” means a person who is not a U.S. person, which is defined in section 7701(a)(30) of the Internal Revenue Code of 1986 as a citizen or resident of the U.S., domestic partnership and corporation, and other estates and trusts

- Has not experienced any change in ownership in the preceding twelve-month (12) period;

- Has not sent or received any funds in an amount greater than $1,000, either directly or through any financial account in which the entity or any affiliate of the entity had an interest, in the preceding twelve-month (12) period; and

- Does not otherwise hold any kind or type of assets, whether in the U.S. or abroad, including any ownership interest in any corporation, limited liability company, or other similar entity.

WHAT: Required Information for BOI Report

Each Reporting Company’s BOI Report must include the following information:

(i) Legal name and any trade or DBA name(s);

(ii) Entity address (usually the principal place of business in the US or primary location in other cases);

(iii) Jurisdiction where the Company was formed or first registered; and

(iv) Taxpayer Identification Number (TIN) and/or Employer Identification Number (EIN).

Additionally, the CTA requires that a Reporting Company’s BOI Report identify all “Beneficial Owners”—defined as any individual who, directly or indirectly, exercises substantial control over the Reporting Company or who owns or controls at least 25% of the Reporting Company – and certain other individuals.

All persons meeting the definition of a Beneficial Owner must provide the following pieces of information:

- Full name;

- Date of birth;

- Address (usually home address);

- An identifying number from a driver’s license, passport, or other approved document; and

- An image of the approved identification document for each individual.

All persons or entities filing a BOI Report or application under the CTA must certify that it is true, correct, and complete. It is estimated that the BOI Report may take three (3) hours to complete.

FinCEN enables Beneficial Owners to apply for and receive a unique identification number associated with that person or entity (“FinCEN ID”). For Beneficial Owners who receive their own FinCEN ID, it can be used in lieu of resubmitting the same information, thereby saving the applicant time when submitting future BOI Reports.

Based on the complex corporate structures involved in many businesses, many Reporting Companies will need to file a number of BOI Reports to comply with the CTA. Therefore, entities and persons are advised to apply for their own FinCEN ID if they (or a Reporting Company with which they are associated) expect to file multiple BOI Reports in the future.

WHEN: Filing Deadlines, Updates and Corrections to BOI Report

Reporting Companies are required to file their initial BOI Report according to the chart below. There is no annual requirement to file a BOI Report, only the initial BOI report. After the initial BOI Report, Reporting Companies are only required to update or correct the report, as information changes.

| Deadlines | |||

| Initial Filing | Updates | Corrections | |

| Pre-2024 Companies | 1 year | 30 days | 30 days from Reporting Company becoming aware or having reason to know of inaccuracy regarding Reporting Company or Beneficial Owner |

| Companies formed in 2024 | 90 days | ||

| Companies formed after 2024 | 30 days | ||

WHY: Penalties(!)

Civil penalties for failing to comply with the CTA are significant and can include criminal penalties. These penalties are compounded where noncompliance is willful.

Reporting Companies who fail to comply with the CTA—willfully or not—face fines of up to $500 for each day that the violation continues. Violators also face criminal penalties, including imprisonment for up to two (2) years and/or a fine of up to $10,000, where there was a willful failure to file or to provide complete or updated information, or fraudulent conveyance of false information.

… Next Steps

1. Consider whether your business may be one of the exempt business categories described above.

2. Identify and evaluate who and what needs to be reported and begin collecting the information—including images of required IDs.

3. Pay attention to the deadlines listed above and exercise diligence when and where previously reported information needs to be updated or corrected. Reporting requirements are ongoing and the penalties for noncompliance are steep.

4. But keep in mind, the CTA is a new law just now taking effect and one which will have unforeseen impacts. The requirements, exemptions, and enforcement mechanisms are not fully tested—and the full impacts are not yet known.

At DP&F, we can advise on CTA requirements as they relate to your business. For more information about the CTA and its impact on your business—or if you plan to form a new business entity—please email Carol Kingery Ritter, John Trinidad, or Owen Dallmeyer.

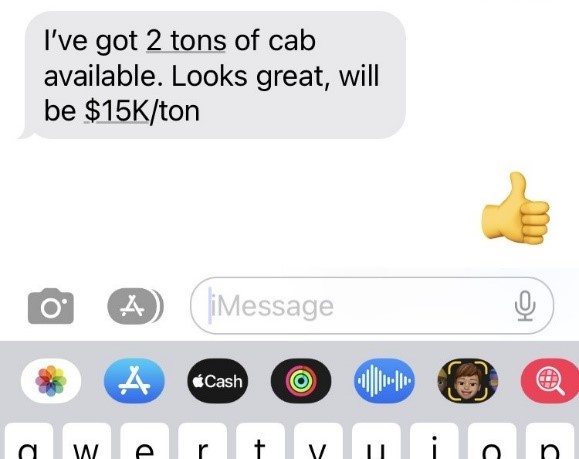

Canadian Court Gives 👍 to Contract Accepted by Emoji

Harvest is underway in wine country. During this season there is increased demand for skilled labor, transportation, and crush facilities. Buyers and sellers of fruit have a short window to make deals. A busy harvest season also lends itself to casual communication about crops, like this:

Now, did you just tell your friend you are happy for him, or did you just commit to buying $30K worth of fruit?

According to at least one Canadian court, the thumbs-up 👍 emoji could qualify as acceptance of a contract. A recent decision from the Court of King’s Bench in Canada discussed the “new reality in Canadian society” facing courts as the forms of communication broaden.

The Canadian court examined a dispute between a farmer and grain buyer over an alleged contract for 87 metric tons of flax, to be delivered in November 2021. The grain buyer and farmer spoke by phone, and the buyer texted the farmer a photo of the contract signed by buyer for November delivery. The text message said “please confirm flax contract.” The farmer texted back a “thumbs-up” emoji.

Later, when November rolled around, the price of flax had gone up, and the farmer attempted to say that his “thumbs-up” in response to the buyer only signaled that he had received the contract, not that he had accepted it. The court also looked at the prior dealings between the farmer and buyer, noting that in prior contracts for durum wheat, the farmer had various formed agreements with the buyer employing similarly concise responses, including “looks good,” “ok,” or “yup.”

Here, the court ultimately found that yes, the “thumbs-up” was sufficient acceptance, and the farmer was ordered to pay C$82,000 for the unfulfilled contract.

Canadian law is not controlling in the United States. However, this case reminds us that as forms and methods of communication grow, U.S. courts may eventually find that an emoji can qualify as acceptance of an agreement.

So, during important business negotiations, consider the potential consequences of casually firing off that “thumbs-up” emoji to the other side. Finally, when in doubt, seek the advice of an attorney.

End in Sight for Temporary Covid Relief Measures from CA ABC

The California Department of Alcoholic Beverage Control announced today end dates for the temporary relief measures announced in 2020 in response to the Covid-19 pandemic. Depending on the specific regulatory relief in question, the relief granted by ABC, and the expanded privileges granted to many licensees during Covid, will come to an end on either June 30 or December 31, 2021.

To assist licensees during the difficulties that arose from shut downs and restricted operations during Covid, the ABC issued various Notices of Regulatory Relief, advising the industry that certain practices would essentially be temporarily permitted With the end of Covid somewhat in sight here in California, the ABC has now provided the end dates for these measures.

The following Notices of Regulatory relief will be rescinded and no longer effective as of the close of business on June 30, 2021.

- Returns of Alcoholic Beverages

- Retail-to-Retail Transactions

- Extension of Credit

- Drive-Thru Windows for Off-Sale Transactions

- Hours of Operations for Retail Sales

- Delivery Hours Extended to Midnight

- Distilled Spirits Manufacturers Providing High-Proof Spirits for Disinfection Purposes

- Virtual Wine Tastings

- Extension of Regulatory Relief for Club Licenses: Type 50, 51 and 52

The ABC is allowing certain items of regulatory relief to remain in place until the end of the year. The following Notices of Regulatory Relief will thus temporarily remain in place until December 31, 2021 and rescinded immediately thereafter.

- On-Sale Retailers Exercising Off-Sale Privileges

- Sales of Alcoholic Beverages To-Go

- Deliveries to Consumers

- Free Delivery

- Expansion of Licensed Footprint

- On-Sale Licensees without Kitchen Facilities

- “Virtual” Meet the Winemaker or Brewer Dinners

- Renewal of Relief for Charitable Promotions and Sales

- Relief from Type-75 Requirement to Produce 100 Barrels of Beer Annually

These changes will have a big impact on industry members who have spent over a year incorporating some of these practices into their sales, marketing and distribution programs. For example, as of June 30, Virtual Wine Tastings with consumers (where samples of wine were shipped to the consumer for the tasting) will no longer be permitted, although Virtual Winemaker Dinners in conjunction with licensed retailers can continue until December 31.

Absent legislative changes to the ABC Act, none of the regulatory relief measures provided by ABC during Covid will become permanent, so licensees should start preparing now to make these shifts. It should be noted that proposals are already pending in the legislature to keep some of these measures in place for the long term. For example, a bill is currently pending that would allow certain licenses to donate a portion of their proceeds to charities, which was previously prohibited.

For more information on what each of the Notices of Regulatory Relief specifically provided, please visit https://www.abc.ca.gov/law-and-policy/coronavirus19/ or contact Bahaneh Hobel.